There is a constant tension in the startup sphere, tech press and sometimes board room between entrepreneurs and VCs. This isn’t surprising considering the fierce confidence and independence required to operate successfully in either role – and given that cash and stock are being exchanged.

Who bears responsibility for the tension? It falls to both sides, but as professional service providers who are permanently in the market, we VCs need to do better. This was highlighted last week in Ryan Caldbeck’s VentureBeat article “Entrepreneurs to venture capitalists: We’re looking for 5 traits.” I could sum up the article in four words: be honest and respectful… or… don’t be an ass hole.

Calbeck’s article was timely for me. I want to really understand what entrepreneurs think of VCs and what VCs think of themselves to be a better VC myself. Time to rev up the survey engine. One survey went to VCs – 58 (mostly partners) answered. Another went to entrepreneurs – 162 (mostly CEO/founders) answered. Not perfectly scientific but directional. VCs, hold onto your seats…

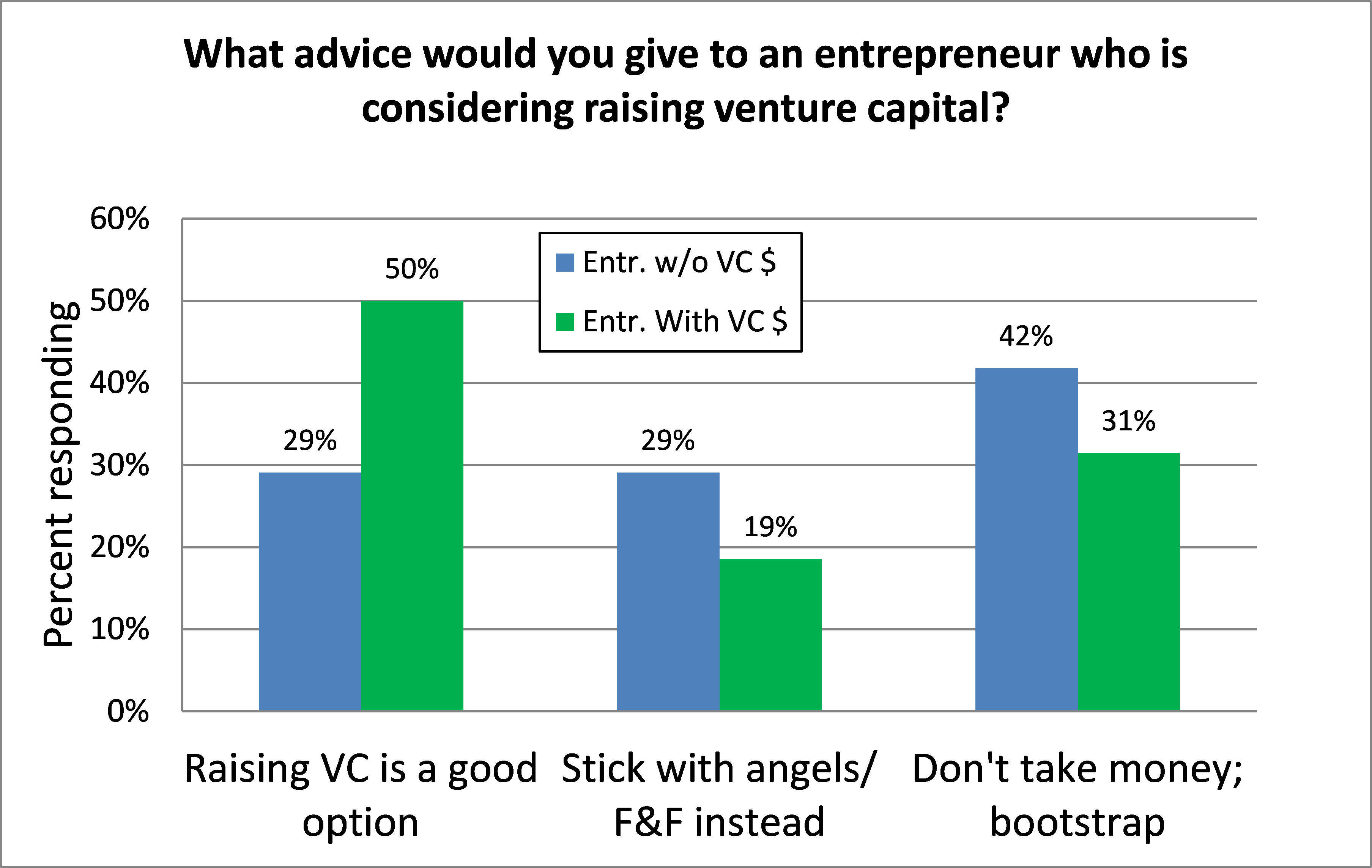

Only 50% of entrepreneurs who took venture capital see it as a good option for others:

It is true that ~75% of venture backed startups fail… so maybe this result is just sour grapes. But I hope that I walk out of my losing VC bets with founder recommendations despite the shared failure. The data below look even worse when filtered for entrepreneurs who haven’t taken venture: fewer than 1/3 of non-venture backed entrepreneurs would recommend venture capital to another entrepreneur. 40% would instead recommend bootstrapping. This is bad for VCs. Some of the deals I most want to be in are the ones who don’t want outside capital. I hope I can convince them.

Hate congress, love your congressperson: 60% of entrepreneurs would recommend most of their VCs, but most entrepreneurs wouldn’t recommend the other VCs they’ve met with

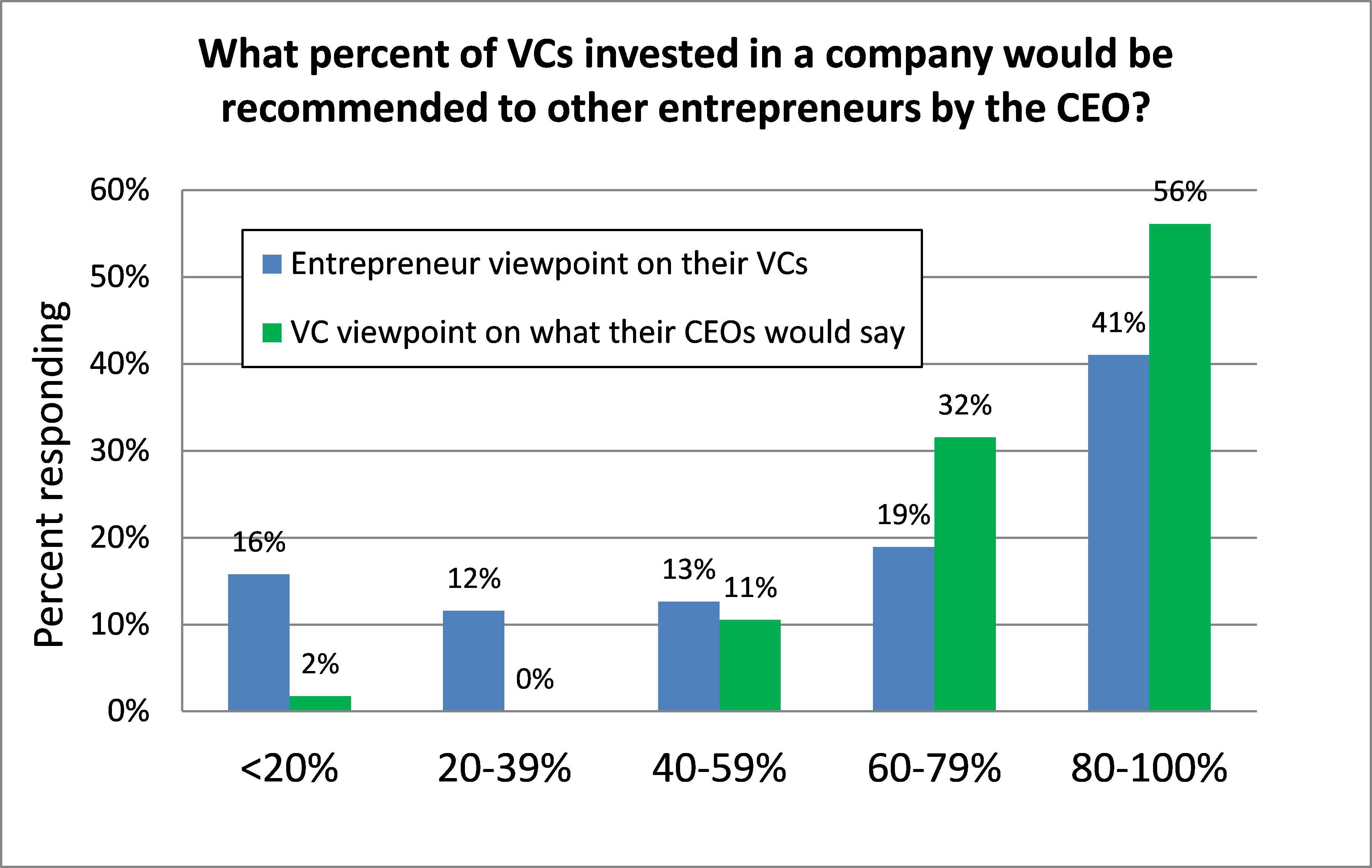

The congress analogy is promising for VCs individually, but even here, we have an inflated self-view of what entrepreneurs think of us:

The above shows that about 90% of VCs would say most entrepreneurs they work with would recommend them, but only 60% of entrepreneurs would likely do it. Why? See below.

While both VCs and entrepreneurs agree it’s because VCs are often viewed as not helpful or not involved, VCs believe a lot of hard feelings tie back to executive firings. Entrepreneurs aren’t actually so caught up with that, but they do think VCs are difficult to work with (ass holes?) at about twice the rate we think we are.

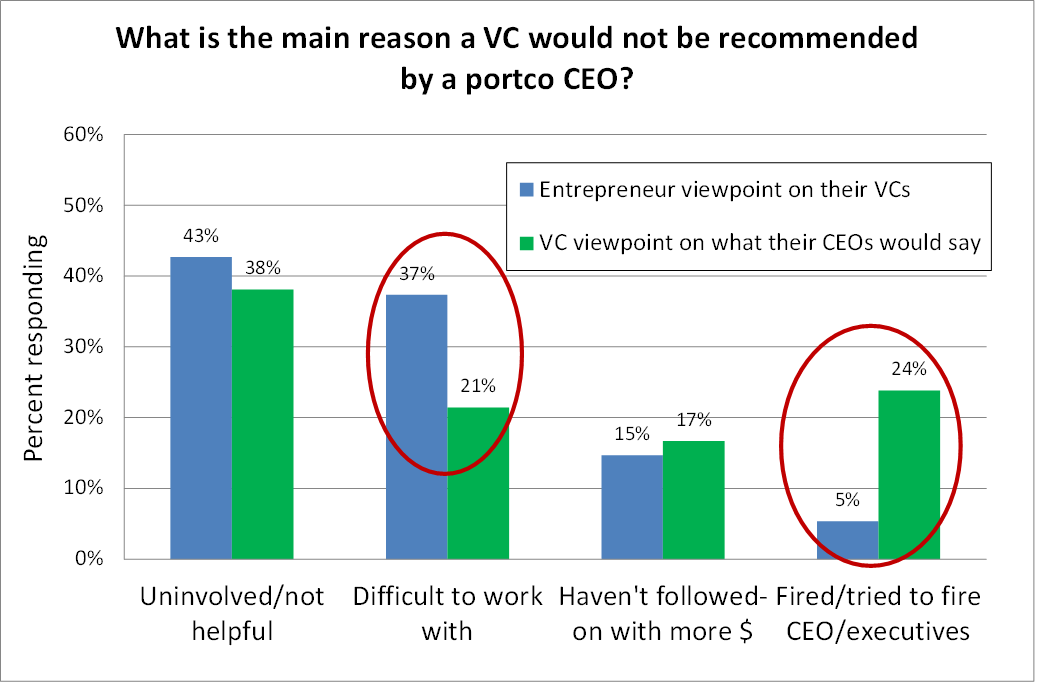

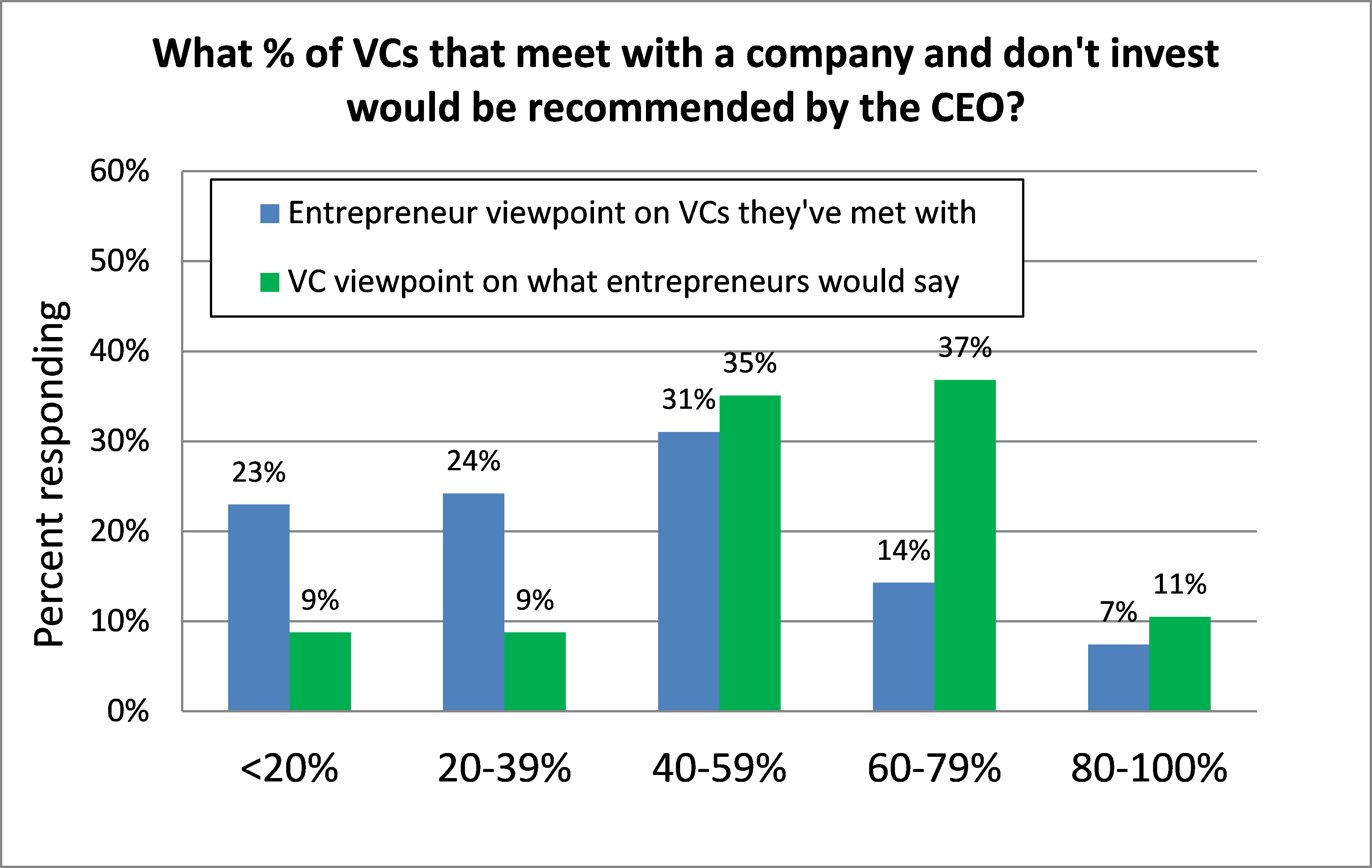

This VC self-awareness issue gets much worse when VCs consider what the CEOs they don’t back would say about them:

About 80% of entrepreneurs would recommend less than half of the VCs they meet, while 85% of VCs think most would recommend them. Here’s why according to entrepreneurs:

Overwhelmingly we come across as arrogant, don’t seem to understand the business or are unhelpful. Yikes. … back to Caldbeck.

This self-awareness disconnect is an unfortunate outcome of how the startup/venture market works. Entrepreneurs rarely give feedback to VCs (though we VCs certainly dish it out). No matter how much an entrepreneur dislikes you, they’re going to ride it out on the chance of getting money from you. Cash is king. There is nothing to gain and lots of risk from giving feedback to a VC – being branded a “hot head” or “difficult founder” in a close knit market. Here’s another way to think about it: VCs are constantly grin f*&%’d, so we think pretty highly of ourselves. To be fair, entrepreneurs are GF’d too but at least for them it can be avoided. VCs can just say “no” faster. Another point of Caldbeck’s.

VCs need to actively solicit feedback to stay in touch with their entrepreneur customers and the market. My colleague Taylor Davidson at KBSP.vc does this with a semi-monthly anonymous survey. Nice.

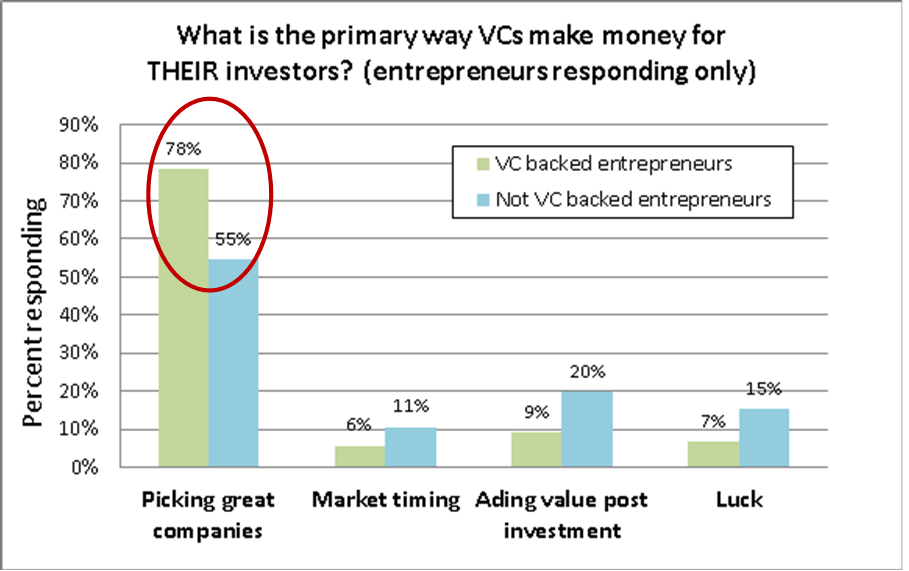

Entrepreneurs’ dissatisfaction comes from misguided expectations set by VCs

When I meet with entrepreneurs, I tell them most VCs overpromise and under-deliver, and I am no different. We all have our moments of adding value – sometimes significant, but when you do the math, how much time does a VC really put into each portco? What really matters is whether a VC and entrepreneur can get along and respect each other when things get tough. Entrepreneurs need to know that we VCs make our money by picking great teams and companies and letting them run – adding value is secondary. VCs overwhelmingly agree with this. On average entrepreneurs seem to understand it too…

…but when you split it out between venture backed and non-venture backed entrepreneurs, you see where the disappointment comes in.

Only 55% of non-venture backed entrepreneurs (eg, the ones looking for money) versus 80% of venture backed entrepreneurs really understand that VCs make money primarily from picking. Making money by picking is not bad. We just need to be honest about what we do and don’t do, know and don’t know so that entrepreneurs aren’t disappointed after investment.

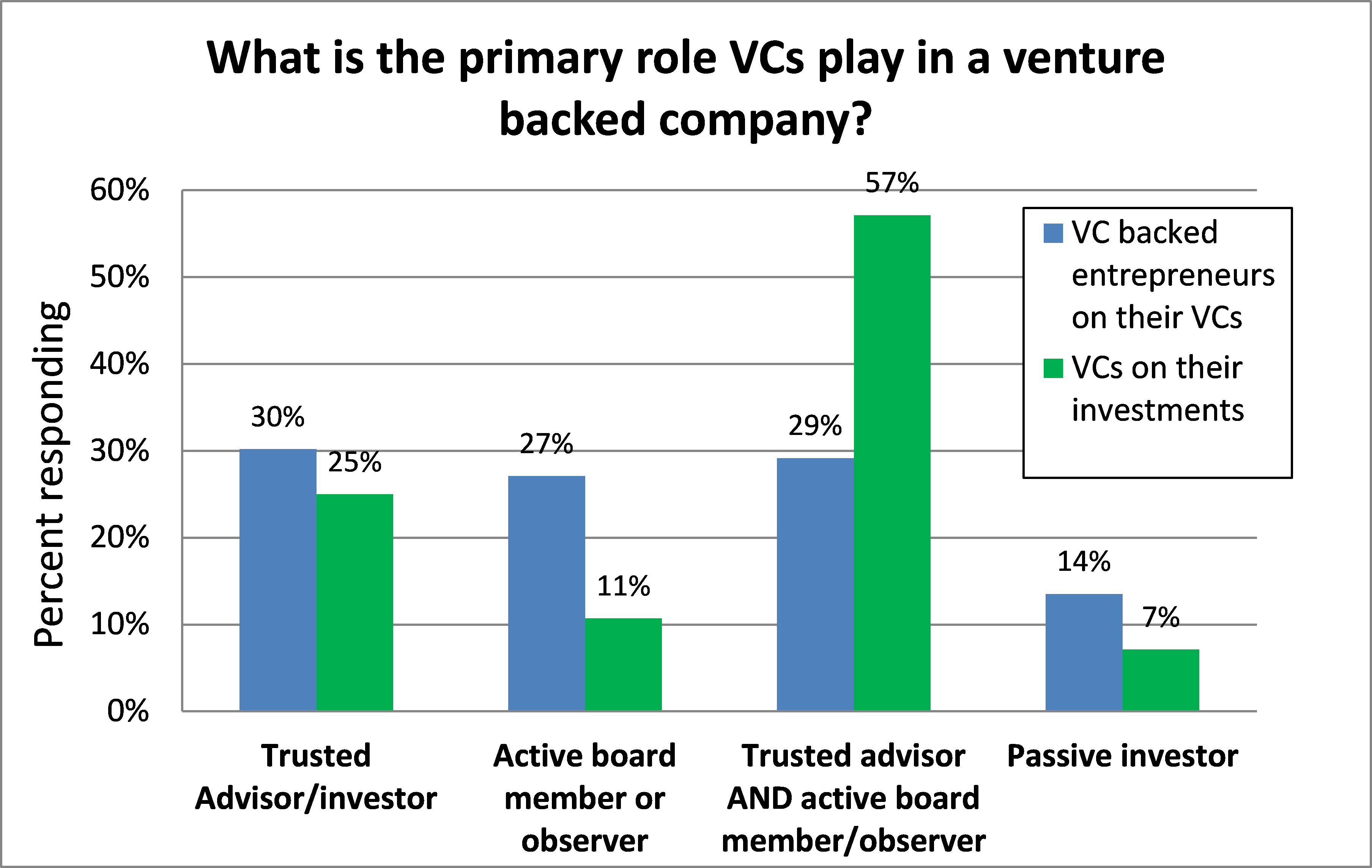

The role VCs play is not as “trusted” as we’d hope

VCs think they are “trusted advisors” in addition to active Board participants at twice the rate venture backed entrepreneurs say so – another VC self-awareness issue.

Why are VCs not as trusted as we think we are? Our interests are usually aligned with the entrepreneurs, but there are times when they aren’t. Our behavior during these times can really turn entrepreneurs off. We need to communicate about what is happening – that we are balancing our obligation to the company and to our partnership, or sometimes forcing hard board decisions on people for overall company results. As one of my portco CEOs said when he was diligencing me: “Every VC flies off the handle at one point or another. So far, I haven’t heard of you doing that, but I expect you will.” I have, in fact, and I am sorry. Not surprisingly, it was a situation where I was caught between a company and my fund. I am lucky that my CEO called me on it, and we worked through it. Most don’t. Bottom line, it’s hard to be trusted when people don’t understand what or why you’re doing something. VCs, communicate.

The good news: we do sometimes add value

While a few venture backed CEOs held out that their VCs don’t add value in any way, most saw some value.

VCs have an inflated view of their 1:1 coaching of CEOs (not surprising) but also underestimate their value in board meetings. This may tie to the ruckus about startup board meetings being useless. VCs and some CEOs may tire of their endless board meetings, but to many entrepreneurs these meetings are important and likely the time when they get the most face-to-face interaction with VCs (like it or not).

VCs, if you are thinking of all the reasons why this is BS, you missed the point

Maybe you are the exception, and certainly some of us are better than others. (Some of us are better at certain times of the day!… we are only human.) But take the feedback, and let’s get better together.

Best content,i am looking for sach a content from long time period, thanku for posting it. It is very great help for me. I never read content like this. Thanku and Keep posting 🙂sweetflirting

Amen!

These days more and more entrepreneurs are fleeing VC funding, to angels, crowdfunding, and bootstrapping. The advent of JOBS Act Title III (when the SEC finally gets its rule-making act together) will accelerate the refugees.

But it’s not all entrepreneurs leaving VC, it’s also VC leaving entrepreneurs. Seems like nothing is of interest except me-too social media and business-model start-ups, that can be popped $100k and flipped for a gigabuck in six months. Right. No wonder the LPs are unhappy. Time was that Sand Hill Road would take on capital-intensive ventures – the steel mill, railroad, and in our case, heavy semi kind of thing. No longer – cap intensive is now in New York, London and Dubai.

So most everyone with a real idea and real talent is bootstrapping if they possibly can. Even cap intensive. We were a *decade* in stealth bootstrap designing our chips – CPU design is not quick. We had no premises, no bank account, no employees – and over that decade accumulated over $10M worth of sweat-equity engineering work. Then the patent rules changed to first-to-file, we put in our 60+ patents, and started taking our technology public with a series of technical presentations. Google “Mill CPU architecture” to see the reaction of the engineering community worldwide.

And I started to get emails “Your work is fantastic – is there any way I can invest?” – from total strangers. We now have a bank account and employees, but still no VCs. We’d be happy to have a VC aboard – we’re sort of a B-C round equivalent at this point – but the deal has to be competitive to what we are already doing, and it’s not clear that required VC margins will admit something like that.

What has happened in the funding industry is a classic disruptor story – high-margin entrenched gate-keepers (the VCs) are faced with low-cost low-margin new entrants (all the kinds of bootstrapping) who are eating their lunch – er, deal flow. I’m not surprised at the graphs in the article – arrogance is an occupational hazard for rentiers of all sorts, be they landed aristocrats or VCs. And the rest of us – peasants or entrepreneurs – will say “Yes, boss” only so long as there is no other choice.

We were very unusual – early (started during the dot-bomb, when we had no choice but bootstrap), cap intensive, very long development time in which money wouldn’t really have made much difference (except personally – ten years without a paycheck is a lot for an engineer). But I see others following our path now, and more all the time.

Ivan

Ivan thank you for the comment! I just tweeted “arrogance is an occupational hazard for rentiers of all sorts, be they landed aristocrats or VCs.” Very memorable comment.

What was the demographic make up of the entrepreneurs and VCs in this survey ?