The common wisdom of venture is that you lose all your money in the bottom third of your companies, score singles to triples in the middle third, and drive the vast majority of value in your top third. A “Midas Lister” we know astutely refines this saying, “It’s actually the top third of the top third where you make all your money”. This seems to resonate with another startup rule of thumb that 1 in 10 investments is a home run.

The problem with these rules of thumb is that a few years into a fund when you are making new investments, following on in existing ones and looking for patterns to determine where to invest time and money before winners are obvious, after-game learnings don’t help you see the future.

It turns out there is a pattern of early warnings we’ve seen in the fifty companies we’ve worked with. The roadsigns to understanding how the thirds **may** break down can be summarized as follows:

- Top third: Top third companies are the ones where everyone is in the same room together (founders/mangement, board, investors), talking about how well sales are going and figuring out how to pour more money on.

- Middle third: Middle third companies are the ones where sales are not going swimmingly, but everyone is still in the same room together discussing how to make them better, either through product, go-to-market or team adjustments.

- Bottom third: Bottom third companies are ones where sales are not going swimmingly, and everyone is in different rooms (calls, coffees) talking about everything except sales.

Upon reading this, entrepreneurs and investors will immediately know where their compan(ies) stand. Don’t worry, I use the word “roadsign” intentionally. This trio of forewarnings allows time to course correct. So how do you do it?

Top third companies are incredibly rewarding for everyone (sometimes fun, sometimes challenging, sometimes stressful… but always rewarding). Revenue is beating plan, talent is flocking in and VCs keep calling. But you can still screw it up. The common modes of failure include: not hire experienced functional leaders to manage scale; not building market leadership, integration and distribution among other key market players; over-focusing on top-line to the detriment of other key metrics like churn and unit economics (eg, growth at all cost); and generally getting over-confident. Even if you avoid these potholes, ultimately landing in the top third of the top third is still highly dependent on market timing and often pursuit of a non-consensus thesis – not just perfect execution.

Middle third companies are really a fat middle, typically representing 50% of a portfolio. Most VCs have lots of these investments, and most entrepreneurs are running one. Things aren’t going perfectly, or sometimes they are going poorly, but everyone is working hard together to figure it out. Getting into the top third from the middle third is about executing well on product and go-to-market strategy in your current market or finding a riper adjacent market space. If these course corrections don’t work with some time, then the next step may be a change in functional or CEO leadership. The latter is traumatic, time consuming and capital consuming. It is a last resort, but in middle third companies when it is done, it is done smoothly with open dialogue between founders, other managers, investors and board members. You continue to row together.

Bottom third companies (actually often about 10-20% of a portfolio) look very similar to middle third companies – ranging in growth profile from slightly downward or flat to moderate growth – with the additional challenge that some combination of people aren’t getting along. This creates significant distraction to solving the root growth issue.

And since the theme of this post is threes, there seem to be three modes of such people challenges:

- Founder – founder: We’ve seen a number of companies handicapped by founder-founder problems, sometimes due to performance issues but more usually personality conflict. If they can’t be worked out, then board members or investors need to quickly help arbitrate – sometimes with the result that one founder moves on.

- Investor/board – management: These scenarios typically result from company under-performance that leads to investors or the board “moving on” a CEO… or the CEO thinking they will. There are also more nuanced instances where performance is good, but there are disagreements over personnel, strategy or ethics. Because investor/CEO relationships can be accompanied by baggage from prior financing negotiations or fear of VCs “stealing my company,” we’ve found that independent board members are critical in helping a company through these times. Independents can play an objective referee and build consensus around a leadership decision, helping the company move to a new chapter whether with that CEO or a different one. Of note, many startups have independent seats on their board that are not filled. This is one reason among many that it is worth filling them ASAP.

- Everyone – everyone: Call this a complicated love triangle without the love, where some investors don’t agree on a key issue with other investors, whom in turn don’t agree with management and independents, etc. Factions form. These are really tough situations (often related to leadership or financing) and require a strong CEO, independent director or Chairman to call bullshit, get everyone in a room together and hash it out. Such fractures generally arise from a difference in economic position or differences in perspectives on people or market – all valid business views. In the end, parties need to commit to eating a little crow and moving forward. The other solution is to sell the company – effectively a divorce – but this is easier said than done. Selling a company requires development of consensus on process and takeout price, no easy feat when people aren’t getting along.

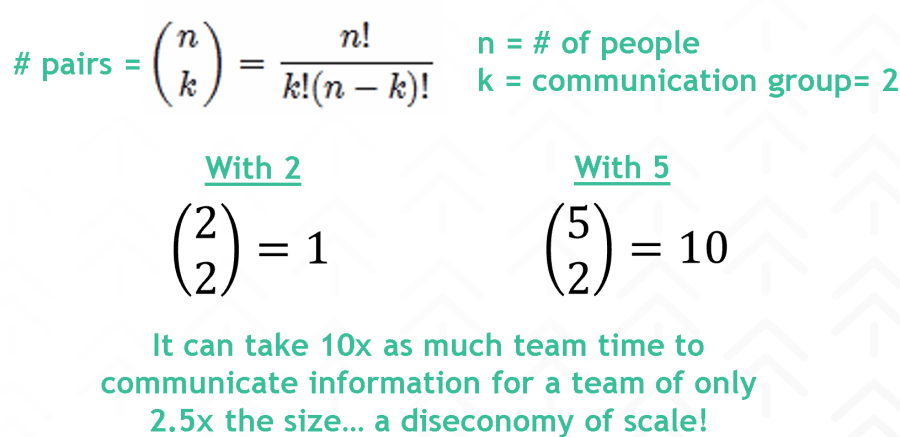

Why are these situations so destructive? Time and emotion are the key factors. A complete set of 1:1 side conversations for a board of five people takes 10 times as much time as a single group conversation (see math below). These conversations are often emotional and exacting, reducing confidence in the company and belief in the opportunity for each individual and VC partnerships involved. Above all, they distract from the underlying issue the company has – usually growth. Growth can’t be fixed unless it has everyone’s focus and a mutually trusting team to pursue it.

As with so many ailments, diagnosis is the first step to recovery. If you and your team/board/investors can recognize a bottom third issue, then you can work to get back into the middle third and eventually to the top!

Fun math on side conversations: