It’s been a bit under 60 days since AngelList announced Syndicates. What do we know so far? Is it really the great venture capital rotation that @jason described? Is AngelList becoming the democracy of funding with successful entrepreneurs funding new founders, angels gaining strength and big bad VC’s pushed to the side? Turns out, not really.

Amidst the defensive VC jabber that ensued the launch of syndicates, @bfeld made a bold move and launched an FG syndicate. Whether Brad tipped the tide or was just a leading indicator, VCs are now playing heavily on AngelList. It is a low cost way to participate in seed deal flow. But not only are VCs seeking participation, capital is actually seeking them on AngelList. Turns out would-be syndicate members are drawn to professional managers. Go figure.

AngelList: (some) VCs in sheep’s clothing

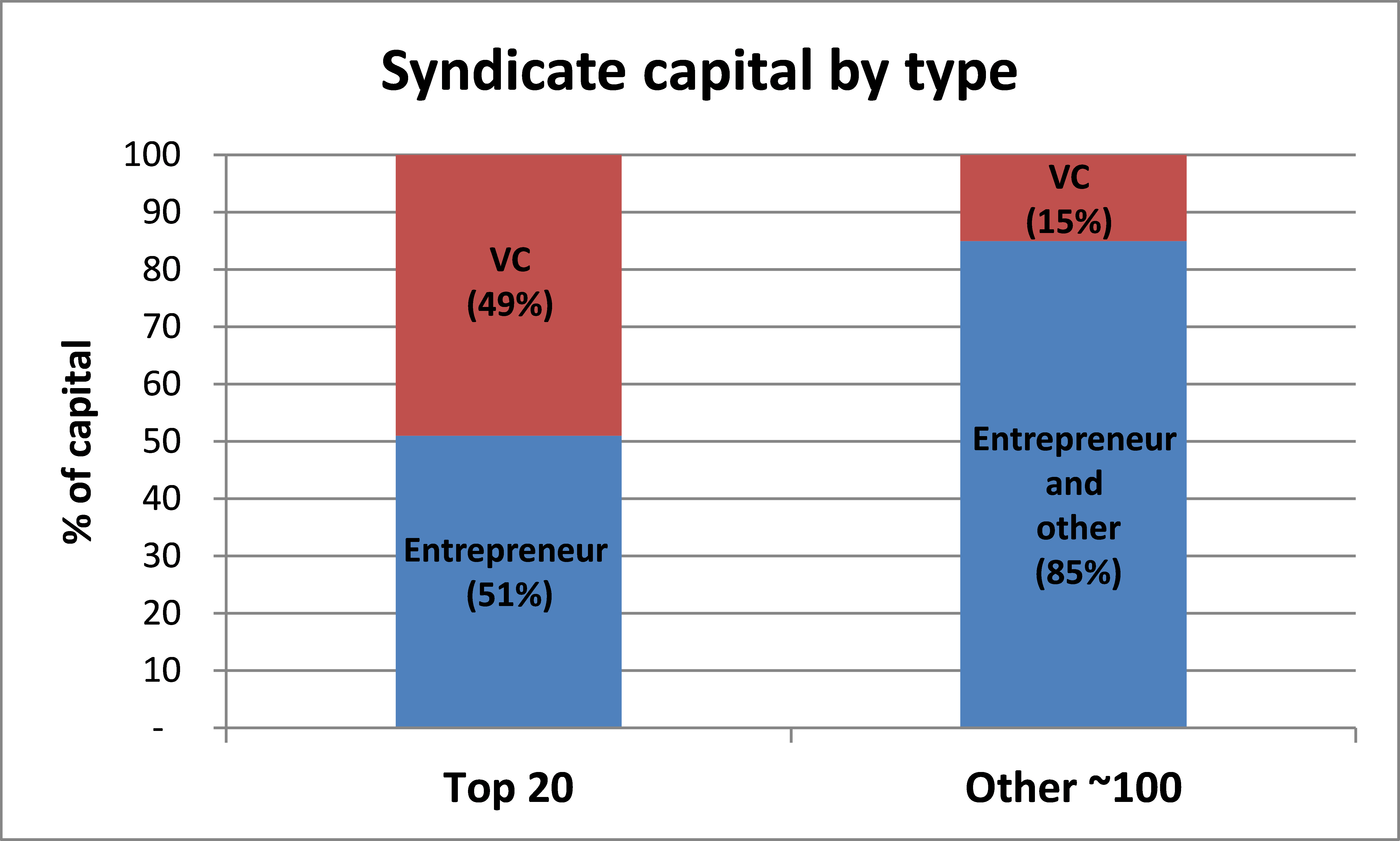

The chart below shows the top 20 AngelList Syndicates as of Nov 5th (note that #1 Kevin Rose has added $400K since then!!!). The distribution of syndicates has a VERY long tail, so these top 20 account for a whopping $8.1M out of $9.9M total. 9 of these 20 are what I call “VC” syndicates – led by a VC or general partner at a venture fund. The rest tend to be successful entrepreneurs. On a capital basis, 49% is “VC” and 51% is “entrepreneur”.

Source: AngelList Nov 5, 2013

Note that there are three Google Ventures GPs in this top 20 – Kevin Rose, MG Siegler, and Wesley Chan. They account for 31% of the syndicate capital. Wow… seems like a pretty strong competitive funding position for Google Ventures, a smart – and likely concerted – move. As usual, Google is everywhere.

The point is that many of the same investors that companies meet with in fancy Sand Hill digs are now cruising for love on AngelList. There are also, of course, renowned entrepreneur angel investors like Tim Ferriss, Dave Morin, Jason Calacanis, and Naval Ravikant who are heavily empowered by the platform too.

This is all a terrific outcome for entrepreneurs, increasing the flow of capital to startups and reducing the transaction costs of landing capital. Contrary to the buzz, however, AngelList is also a boon for VCs who choose to ride the wave… as we can see by Google Ventures’ market position. Even my own fund, Hyde Park Venture Partners, dipped a toe with my partner @iraweiss backing FG’s syndicate. We don’t have enough brass, time or capital to do one ourselves, but we’re excited to learn with Brad.

Capital flows to expertise, time and access

There’s something else these data are telling us. Investing successfully in young companies takes expertise, time and access. The capital is flowing to people who are “proven” along these dimensions – in many cases VCs – not just any angel investor. Shown below, while nearly half of the top 20 syndicate capital is “VC” led, only 15% of the tail capital fits this bill. Viewed through another lens, successfully formed syndicates (the top 20 all have at least $60K in capital, the tail median is a measly $12K) are much more likely to be VC led. Maybe we should call it VCList.co. I’ll have to check GoDaddy for that.

Source: AngelList Nov 5, 2013

For all you haters: Yes, I am a VC. I get it, I’m biased. The analysis also isn’t perfect because it only looks at syndicate formation, not capital velocity. Impact to startups could skew differently than the formation distribution if, say, the “entrepreneur” syndicates invested more often than the “VC” syndicates. But I think you get the point.

I backed Kevin Rose because: (1) he picks a lot of unicorns (2) he’s a partner at Google Ventures, which invests in great startups like Nest, Uber, and (3) he charges no fee and no carry. There’s a 5% carry that goes to AngelList. I’m also a limited partner in a fund that only invests in YC startups, managed by top-ranked FundersClub. The fees are .5/20. Your fees, if you are a standard VC, are at least 2/20. Mattermark may rank you much lower than FundersClub. And your minimums are ridiculously high. Also, you have capital calls. As soon as Kevin Rose goes off the reservation and puts me in a bad startup, I can fire his ass. With a VC, I’m stuck.

All I get from VC limited partners – whether from top endowments or from individuals – are complaints about lack of liquidity and zero alpha.

For me to invest in FundersClub or to back a top AngelList Syndicator is a no brainer, compared to a traditional VC.

It’s just a better business model.

And with $3 million of backing per deal, Kevin can look at Series B rounds – not just seed and A – in light of the Series A and B crunch.

Tell me where I’m wrong.

Thanks for the great thoughts! I don’t think you are wrong. Cost of entry is much lower and ease off access is much higher for investors. This is good for LPs in many circumstances. But what are the risks for LPs?

I question whether top VCs leading syndicates without carry are going to put in the post investment effort that may have contributed to some of their terrific outcomes in the past. They certainly will if their large fund later invest in the deal, but without that, why would they? This also gets to how much value you think VCs create in “picking” versus post investment value add. Lots of opinions on this. If you think VCs create all their value for LPs in picking, then the arrangement probably works well. Except we might also ask whether VCs with syndicates will be as careful about the picking in the AngelList structure! Unlike in their funds, there is no downside in a bad pick except their own small investment loss, which is meaningless for very successful VCs.

Bottom line, what syndicate LPs are doing in big VC’s syndicates is helping to fund the VC’s deal flow for their large funds. That may work out great. It may not. It takes a long time to figure it out. So by the time an LP figures out their VC syndicate lead isn’t doing a good job, there is probably already a lot of money to work and at risk.

Just some thoughts. No rights or wrongs on this. The outcomes will be very volatile as they always are in venture. Some folks will look like geniuses, and the rest probably lose money. This is venture in any form.

Absent so far is a discussion of whether this is all good for entrepreneurs. More options for funding definitely. True access to these rockstar syndicate leads? Maybe.

Or another way to look at it is; while everyone is talking about the doom and gloom for VCs because startup investing is moving faster than the pace they are *said to be* used to, that VCs are actually pretty darn good at adapting to this fast moving ‘investment-platform’ based world.

As the saying goes – You could fight them, join them or in this case ‘become them’…