Crowdfunding, ICOs and COVID. What do these have in common? All three have at one point or another been described as a deathblow to venture. Venture has and will survive all three of these. While we’re in the early innings of the pandemic, an initial freeze in venture has thawed, even if at a more tempered cadence. VCs are screaming on twitter that they’re open for business, and even we have a signed TS with a company right now, so we can scream too.

But should startups take venture in 2020? That is a more complex question. Paul Graham’s much cited and seminal piece Startup = Growth is a great reminder of what venture capital is for: to fund rapid, steep growth. The cost of venture capital is high. Often cited as a 20-30% APR – a reasonable approximation for the average cost of capital for “successful” VC funds – the true cost to an entrepreneur who succeeds can be as high as 100% APR or more. Remember, if you succeed wildly, you have to cover the costs of your VCs’ failures. Now, if that’s the case, you are probably much richer than the VC in the end, so it was worth it. Now back to the growth…

Raise your hand if you have rapid, steep growth in 2020. Uh huh. Most startups will have a terrible 2020 in startup = growth terms. We expect the majority of our companies to fall between a -25% decline (for some consumer and B2B transactional businesses) to a +50% (for stickier SaaS businesses). We are also lucky to have a few “COVID bump” outliers. More on that below.

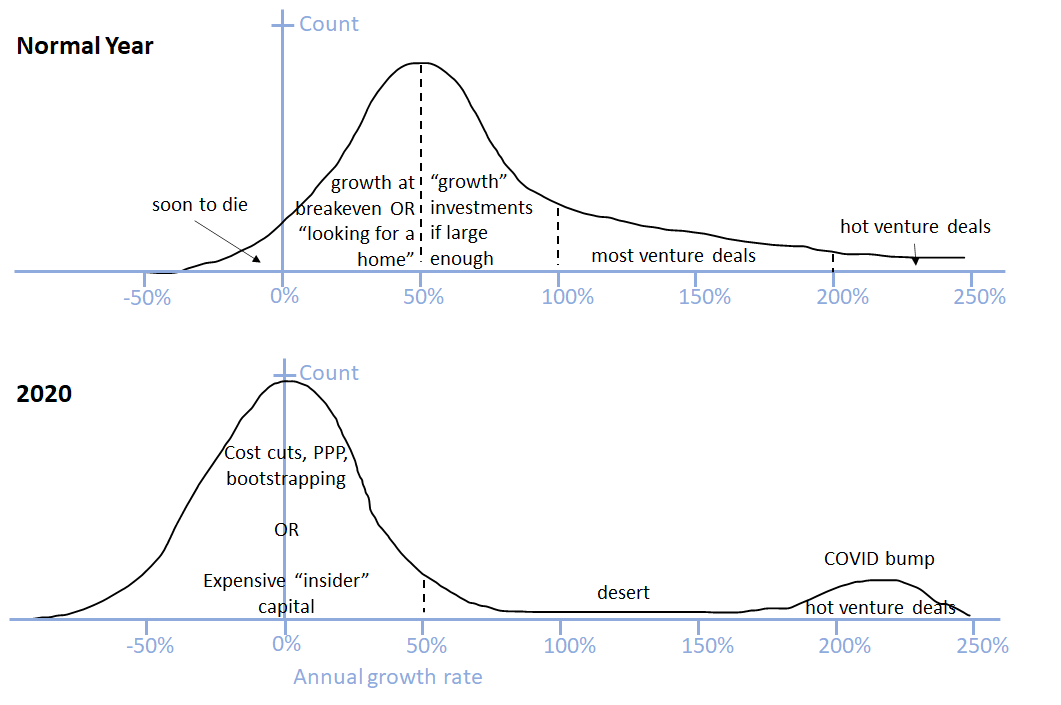

When you’re swimming, it’s good to know where the rest of your pod is. Here is how we see the growth profile of startups in normal times and in 2020. Don’t get caught up on exact numbers, business model etc. This is meant to be illustrative:

In normal times, we see lots of startups growing 25 to 100% annually. Few of these get funded unless they have bulky ARR (say 5M and above), in which case they oftend find a “growth” investor with the right appetite. Then there is a decreasing tail towards and above 200% annual growth. Most venture deals get done in this range with “hot” deals above 200% growth.

In 2020, this distribution has shifted left, roughly centered around 0% growth, maybe slightly above. Then there is a long desert to a small second mode of “COVID bump” companies, where the hot deals are getting done now. These tend to be in e-commerce, virtual care, remote collaboration, online education… you know, the obvious. They get a lot of buzz and are exciting, but most of the announcements you see are companies receiving supported from insiders.

Venture capital is not for survival. It is very expensive if things work out later, so if you’re in the middle of the pack now, do your best to avoid taking venture until you emerge on the other side. Barring the fortune of being in the COVID bump – where pouring gas on the fire makes sense – I’m convinced that the best companies and happiest founders will be the ones who bootstrapped through 2020.

71 thoughts on “Bootstrapping 2020”