The theme for tech in the 2020s is that macroeconomics matter a lot, seemingly much more so than in the prior decade. This makes sense given the mainstreaming of tech and its significant composition of overall GDP as compared to a few decades ago. In this new decade, first pandemic fear, then pandemic elation and now a potential recession is shaking tech back and forth.

When a president says that a recession is not inevitable, we should assume he or she means they are expecting one but hoping their mightiest that it doesn’t happen. I’m pretty sure it’s coming, and here is why.

With inflation increasing – which it has nearly without stop for the last nine months – a recession is not a bug of the Fed’s interest rate hikes; it’s a feature! That is especially true when so much inflation is tied to food and fuel, whose supplies are under duress from the Russian war and over which the Fed has no direct control. The only tool the Fed has is to reduce demand for those and other key economic inputs, e.g. labor. That means hiking interest rates enough to reduce business growth and demand… to drive layoffs… to reduce sticky wage inflation and consumer demand… and so on. Again, recession is not a bug; it’s a feature!

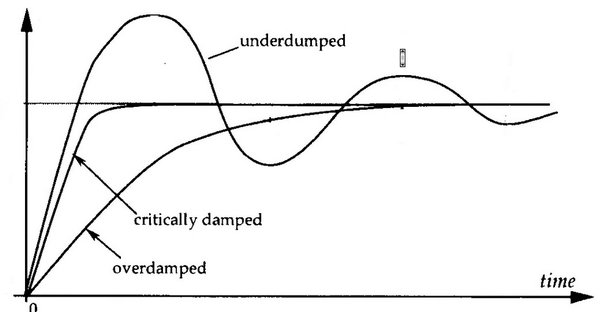

While it’s true that there is a very narrow possibility of a perfect soft landing without recession, that seems unlikely. Interest rates are a rough and imperfect tool, and the overall economy much more resembles an underdamped system in systems theory (see below) than a precisely controlled overdamped system. In an underdamped system, responses tend to overshoot the target.

It’s hard to tell yet how painful a recession will be, so let’s look at housing as an indicator. As a veteran of the financial crisis, I wince when I hear 30 year olds boast about their newly purchased pandemic house increasing in value at 20% a year. History has a short half life. Many retort that this time is different because the financial crisis systemically hampered supply for a decade leaving the US short of millions of homes, while at the same time, people now want more space because of work-from-home needs. Okay, fine, but:

Housing prices = f(supply, owner/occupier demand, input prices, investor demand, interest rates, unemployment, etc, etc)

Over the last two years, most of these variables have been strong tailwinds to housing prices, but some are switching direction now. Yes, supply/inventory will continue to lag, but a simple domino effect could heavily outweigh that:

High interest rates >> reduced consumer buying power >> reduced investor demand >> increased unemployment >> reduced owner/occupier demand>>and so on

In the extreme case where unemployment gets into the upper single digits, a lot of homes with inflated valuations could be foreclosed and later dumped into the market via bank auction. The resulting lower prices only circularly fuel themselves – the catalyst to price collapse during the financial crisis. Will that happen again? Probably not to the extreme, but don’t count on housing prices continuing upward. Psychologically, expectations that housing prices may flatten or drop will also reduce demand by reducing FOMO!

As an allegory for startups:

So if you’re a founder wondering why existing and potential investors are getting more rigid about valuations, think about our housing price example above as an analog.<p style=”padding-left:25px;”>Your text </p>

Startup valuations = f(supply, team experience, investor demand, interest rates, acquisition demand, etc, etc)

Supply doesn’t seem to be changing much initially, but a weaker labor market will eventually free up more and more experienced founding teams. Meanwhile investor demand is down partially because interest rates are up. Explicitly, increasing interest rates have reduced public multiples for valuation comps and made capital harder to raise for VCs, or at least there are expectations that they will. Finally, acquirers also have a higher cost of capital, less valuable stock (currency) and expectations of a recession. They are less likely to buy or buy for high prices.

While much of this sea change is already quantitatively measurable, especially valuation multiples, don’t forget the psychological component. The trends above show that investors have good reasons to believe that prices will fall, reducing FOMO. Some investors may in fact be “scared” by the environment, but more likely they are being pretty rational by waiting.

For example, a post-launch seed stage company in Chicago in 2021 might have raised $3M on $12M. An investor who liked the team and idea/market was likely to think, “okay, I can put $1.5M in now and own 10%. Otherwise, the next round is likely to be $8M on $25M if things go well, which is beyond me. Better to get in now.” Today that investor is probably willing to bet that the company will be back around in a year raising $4M on a flat $15M pre-money with more progress, so the VC will just wait. Alternatively, the VC might be attracted if the seed price was instead $2M on $6M. This waiting, in turn, actually reduces demand and so prices. The circle will not be unbroken.

Does any of this matter? Yes and no. Many companies need capital to grow fast at the early stages. Not everyone needs high valuations to boost their ego, though, and in the new paradigm, startups can raise smaller rounds to manage dilution at lower prices. The changing market could also mean depressed exit valuations, which make a big difference to founders and investors. However, calling the ball on an exit market many years from now is futile.

The real challenge is that we can’t all go hide under a rock until money gets cheap again. At the beginning of the pandemic (before it turned out that tech would flourish), the advice was to cut burn significantly and survive. The expectation was that we could all emerge 6 to 12 months later with a common excuse and start growing again. While it turned out the excuse wasn’t needed, no such excuse exists this time around. The bar for performance stays the same; it’s just that we either have to take more dilution to use the same burn to hit the bar, or burn less to hit it. Both of these are hard in different ways.

One thought on “Recession is a feature, not a bug”