In March the consensus among venture investors – especially ones who had witnessed the .com boom, financial crisis, or both – was that dark times were ahead. Sequoia and others quickly warned their portfolios to significantly cut expenses in expectation that demand would disappear, in most cases regardless of industry or business model type. We did too.

Now almost six months later, the new narrative is that things didn’t turn out as badly as we thought. As evidence, startup financings remained relatively robust in Q2 and into Q3, there has not been a second wave of tech layoffs (and hiring has even restarted) and most companies are seeing a return of demand, albeit often at a muted level.

So did everyone overreact in March? I don’t think so. On the one hand, returning demand is a great thing, on the other hand, there are signs of a structural disequilibrium between main street, public stocks and the startup/venture market. There is also a foreboding sense of complacency with truncating cash runways in many venture portfolio companies.

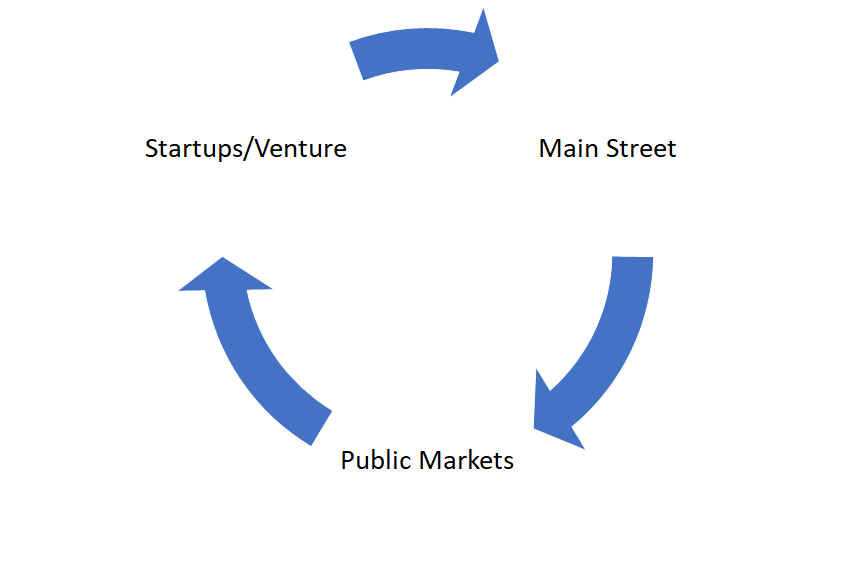

Main street, public markets and venture/startup markets are interdependent, more now than ever given ubiquitous reliance on software, internet and technology across the economy. This was much less so the case in 2000, or even 2008. Today the link is tight:

Main Street: Main Street is hurting. Literally. Wade through the pile of Amazon and Instacart deliveries at your door and take but a few steps to realize small business, restaurants and many services through every city and town are in the shit. While government stimulus has helped – and we can likely expect more – it only puts food on the table and doesn’t yield the confidence consumers need to drive demand. Many startups sell to main street consumers or to the businesses that sell to them, so demand in most industries is undeniably muted.

Public Stocks: It is said that main street is today and the stock market is tomorrow, and this explains why employment can be down 600 basis points in 6 months while stocks return to previous highs over the same period. Okay, if that’s true then we might ask, “will the future (2021, 2022) be as good as 2018 and 2019?” That seems unlikely. Even if we had a vaccine today, the rest of demand and employment recovery is likely to take years, as it usually does following a recession. I am not a market timer, but right now it feels like the market is over-handicapping a quick vaccine and recovery.

So where does the venture/startup world fit in? In the end, public markets represent both a major input and output to the venture/startup model. Most funds invest money from institutional investors who hold a bulk of their holdings in public stock. When those go up, institutional investors “allocate” more to venture; when public stocks go down, those investors “allocate” less to venture. The public markets are also a major exit path for startups, both through direct IPO and M&A to public companies. When the markets drop, both paths deteriorate. So if the market drops again, which seems likely, there will be less money going into venture funds and fewer paths to exit for startups (or at least at lower exit multiples).

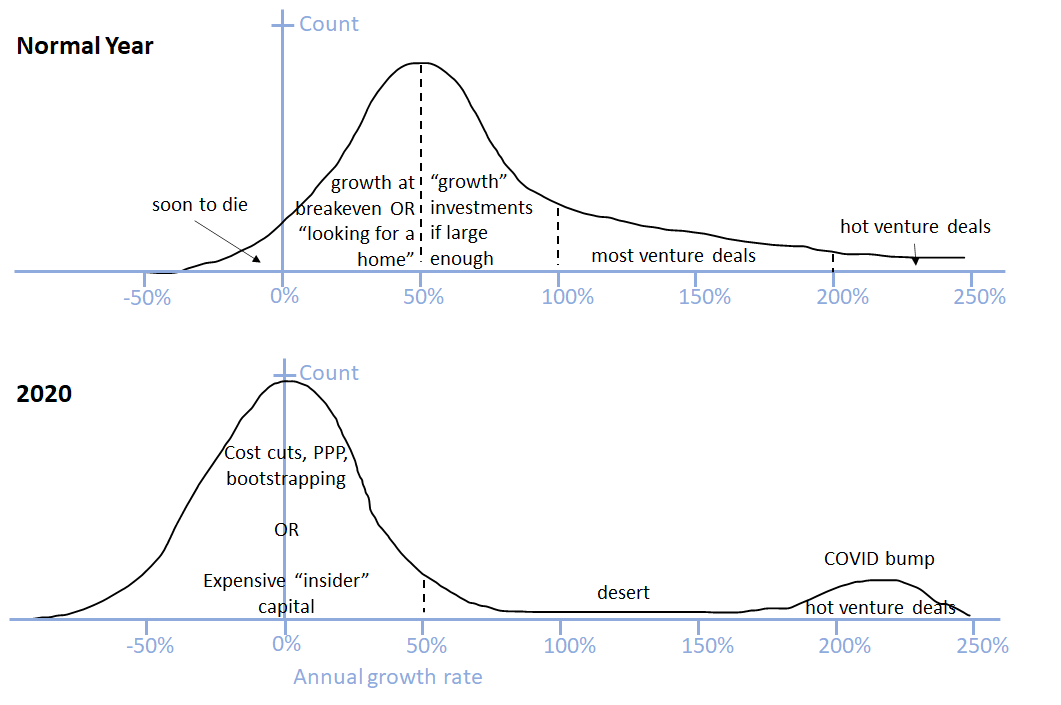

Admittedly, the above cycle is incredibly “macro” and “on average”, while startups and venture funds live by the power law. If you’re lucky enough to be a “COVID bump” startup or to have a few in your portfolio, that is terrific. However, the majority of startups are now growing slowly (in venture terms), chewing through the limited runway they worked hard to extend in March and April. This is what I refer to as the ticking time bomb of venture and startups. These runways expire en masse between late 2020 and mid 2021.

As happened in March and April when VCs focused inwards, I anticipate a recurrence of inward preoccupation when this corpus of slower growing startups become “workouts”. Entrepreneurs and investors will have to pick winners and losers. This will lead to much fallout in existing portfolios but perhaps also a muting in excitement for funding new startups – at least for some time. (It will also be a good time for strong startups to buy weakened competitors and win their customers.)

You can’t be a VC without being an optimist, and I do believe tech is performing and will come through the other side of COVID stronger than ever. But we need to remember that everything is linked, and the current disequilibrium may yield to more pain in the short term.